You have received a large sum — a bonus, an inheritance, or maturity proceeds — and you want to invest it in equity mutual funds. But you are nervous about putting it all in at once. What if the market falls right after you invest? This is exactly the problem that a Systematic Transfer Plan (STP) solves. It lets you invest a lump sum safely and move it into equity gradually, combining the safety of debt with the growth of equity.

What is STP (Systematic Transfer Plan)?

A Systematic Transfer Plan, or STP, is a facility that allows you to transfer a fixed amount from one mutual fund scheme to another at regular intervals — typically monthly. Most commonly, investors park a lump sum in a liquid or debt fund and set up an STP to move a fixed amount into an equity fund every month.

The fund house handles the transfer automatically. Each month, it redeems units worth the STP amount from the source fund and invests that money in the destination fund. You do not have to do anything manually after the initial setup.

How Does STP Work? A Step-by-Step Example

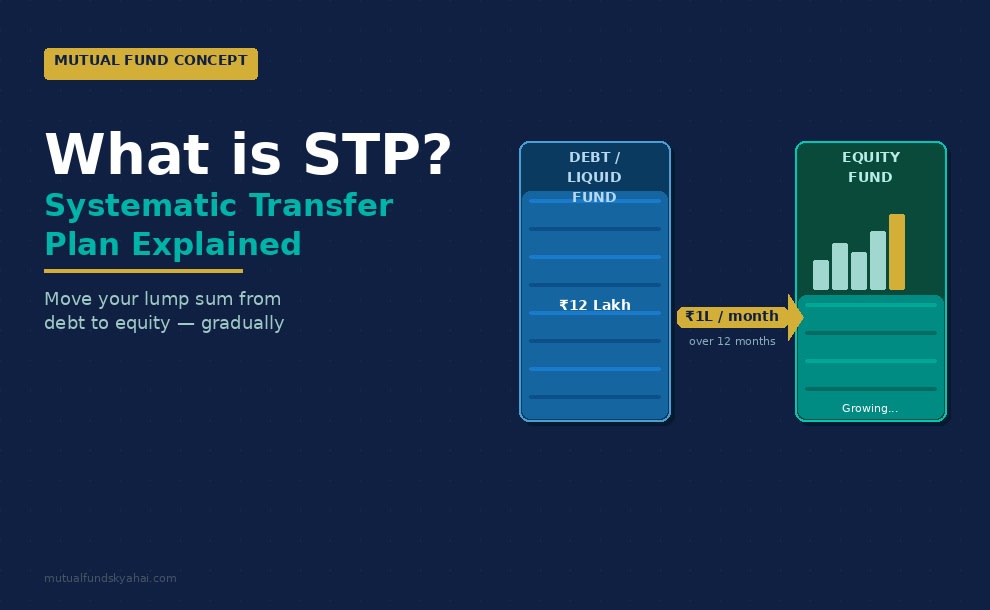

Here is a practical illustration:

- You receive ₹12 lakh as a bonus and want to invest it in a large-cap equity fund.

- Instead of investing all ₹12 lakh at once, you park the entire amount in a liquid fund (say, Fund A).

- You set up a monthly STP of ₹1 lakh from Fund A to a large-cap equity fund (Fund B).

- Over 12 months, ₹1 lakh moves to the equity fund each month. The remaining amount continues earning returns in the liquid fund.

- You benefit from rupee cost averaging in equity, and your idle money earns ~6–7% in the liquid fund while waiting.

The net effect is similar to running a SIP, but the source of money is a fund you already own, not your bank account.

Types of STP

Fixed STP

A fixed rupee amount transfers every period. This is the most popular type, easy to plan and predict. Example: ₹50,000 every month from liquid to equity fund.

Flexi STP

The transfer amount varies based on the performance or valuation of the destination fund. When equity valuations are low (markets are down), a higher amount transfers automatically. When valuations are high, a lower amount moves. This is more sophisticated and requires the fund house to support it.

Capital Appreciation STP

Only the gains made in the source fund are transferred to the destination fund. The principal stays untouched in the source scheme. This is useful if you want to protect your principal but still put growth to work in equity.

Who Should Use STP?

- Lump sum investors: Anyone who has received a large amount at once — salary arrears, property sale proceeds, FD maturity, retirement corpus — and wants to shift it into equity without timing risk.

- Risk-averse investors moving to equity: If you are new to equity funds or uncomfortable with market volatility, STP lets you enter gradually rather than all at once.

- Investors nearing a goal: You can also use STP in reverse — moving from an equity fund to a debt fund as your financial goal approaches, systematically reducing risk.

- Bonus or windfall recipients: Corporate employees who receive annual bonuses or ESOPs can use STP to deploy proceeds efficiently.

Key Things to Watch Out For

- Tax on every transfer: Each STP transfer from the source fund is treated as a redemption and is subject to capital gains tax. For liquid/debt funds, gains are taxed at your income slab rate. If you transfer too frequently or in large amounts, the tax drag can be significant. Plan with your tax advisor.

- Exit load in source fund: Some debt and liquid funds charge an exit load if units are redeemed within 7–30 days. Check the source fund's exit load clause before starting an STP — you may need to stagger the start date.

- Both funds must be with same AMC: STP is an intra-AMC facility. You can only transfer between schemes offered by the same fund house. You cannot do an STP from HDFC Liquid Fund to SBI Bluechip Fund, for example.

- Minimum transfer amounts apply: Most AMCs require a minimum STP amount (often ₹500–₹1,000 per instalment). Ensure your setup meets the fund house's requirements.

- STP is not a SIP substitute: STP uses existing investable money; SIP creates fresh investment discipline from income. Both have different roles. STP is ideal for deploying a corpus; SIP is ideal for regular income earners building wealth.

Frequently Asked Questions

Is STP better than investing a lump sum directly in equity?

It depends on market conditions. In a rising market, a lump sum investment would have performed better. In a volatile or falling market, STP protects you from putting all your money in at a peak. Since market timing is nearly impossible, STP is generally the safer and psychologically easier choice for large amounts.

Can I stop or modify an STP midway?

Yes. Most AMCs allow you to pause, modify the amount, or cancel an STP at any time without penalty. Contact your fund house or use their online portal to make changes.

What is the difference between STP and SIP?

In a SIP, money flows from your bank account to a mutual fund. In an STP, money flows from one mutual fund to another. SIP builds a corpus from regular income; STP deploys an existing corpus more efficiently.

Does the source fund have to be a liquid fund?

No — though liquid funds are the most common choice due to their stability and negligible exit load after 7 days. You can use any debt fund, ultra-short-duration fund, or even a balanced fund as the source, depending on your risk tolerance and investment horizon.