If you have built a mutual fund corpus over the years and now want a regular monthly income from it — without selling your entire investment at once — a Systematic Withdrawal Plan (SWP) is the tool designed exactly for you. It is one of the most practical and tax-efficient ways to generate steady cash flow from your investments.

What is SWP (Systematic Withdrawal Plan)?

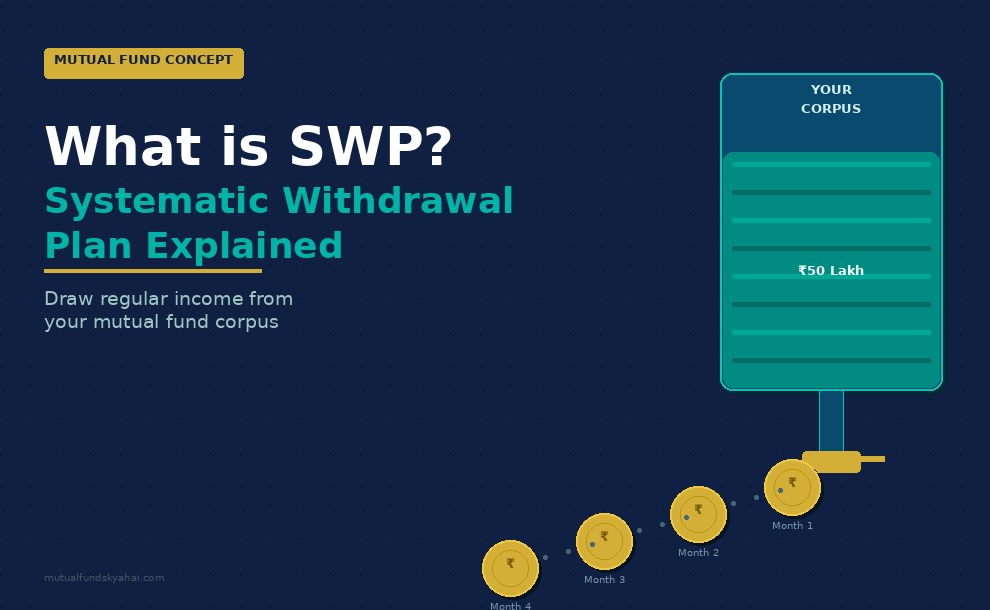

A Systematic Withdrawal Plan, or SWP, is a facility offered by mutual funds that allows you to withdraw a fixed amount from your investment at regular intervals — monthly, quarterly, or annually. Instead of redeeming your entire investment in one go, you instruct the fund house to redeem only a small number of units each period to pay you a predetermined amount.

Think of it as the opposite of a SIP (Systematic Investment Plan). While SIP helps you invest regularly and accumulate wealth, SWP helps you draw down that wealth regularly while keeping the rest invested and growing.

How Does SWP Work?

The mechanics of SWP are straightforward. Here is a simple example:

- Suppose you have ₹50 lakh invested in a balanced advantage fund with a current NAV of ₹100. You hold 50,000 units.

- You set up a monthly SWP of ₹25,000.

- Each month, the fund redeems enough units to pay you ₹25,000. If the NAV that month is ₹102, it redeems approximately 245 units (₹25,000 ÷ ₹102).

- Your remaining units continue to stay invested and participate in market growth.

Over time, if your fund grows faster than your withdrawal rate, your corpus may actually increase or remain stable even as you draw income. This is the power of SWP done right.

Types of SWP

Fixed SWP

You withdraw a fixed rupee amount every month (e.g., ₹20,000). The number of units redeemed varies based on the prevailing NAV. This is the most common type and is ideal for people who need a predictable income.

Appreciation-Based SWP

You withdraw only the gains — the amount by which your investment has grown since the last withdrawal. The principal remains intact. This is more conservative and is suited for investors who want to preserve their corpus while earning some income.

Fixed Units SWP

You redeem a fixed number of units each period. The rupee amount you receive varies with the NAV. Less common, but sometimes used for specific tax planning needs.

Who Should Use SWP?

- Retirees: SWP is an excellent alternative to annuities. It offers flexibility, better post-tax returns, and keeps your money in a diversified portfolio.

- Regular income seekers: Freelancers, consultants, or anyone without a fixed monthly salary can use SWP to create a salary-like cash flow from their corpus.

- Parents funding regular expenses: Whether it is a child's school fees, EMI support, or monthly household costs, SWP can be timed to meet these recurring needs.

- Investors in the distribution phase: Anyone who has accumulated a large corpus through SIP and is now transitioning to a "live off your investments" phase.

Key Things to Watch Out For

- Withdrawal rate matters: If you withdraw more than your fund earns, your corpus will erode over time. A sustainable withdrawal rate is generally considered 4–6% per annum of the corpus, depending on the fund type.

- Tax on each redemption: Every SWP redemption is treated as a sale of mutual fund units and is subject to capital gains tax. For equity funds, short-term capital gains (units held less than 1 year) are taxed at 20%, and long-term gains (over 1 year) above ₹1.25 lakh per year are taxed at 12.5%. For debt funds, gains are added to income and taxed at your slab rate. Plan your SWP with your tax advisor.

- Exit load: Some funds charge an exit load if units are redeemed within a certain period (typically 1 year for equity funds). Structure your SWP start date to avoid this, or choose a fund with no exit load for withdrawals.

- Fund selection is critical: SWP works best with relatively stable or hybrid funds. Withdrawing from a volatile pure equity fund during a market downturn can force you to sell more units at lower NAVs, accelerating corpus erosion.

- Review periodically: Revisit your SWP amount at least once a year. If your corpus has grown significantly, you may be able to increase the withdrawal. If markets have fallen sharply, consider temporarily pausing or reducing the SWP.

Frequently Asked Questions

Is SWP better than the dividend option in mutual funds?

In most cases, yes. The IDCW (dividend) option is not guaranteed and depends on the fund declaring a dividend. SWP, on the other hand, gives you complete control over the amount and timing of your income. Taxation is also generally more favourable with SWP for long-term investors.

Can I stop or change my SWP?

Yes. Most fund houses allow you to pause, modify, or cancel your SWP at any time through their website, app, or by submitting a request. There is no penalty for changing the SWP amount or frequency.

What is the minimum SWP amount?

This varies by fund house, but most AMCs in India allow SWPs starting from ₹500 to ₹1,000 per month. Check the specific scheme's terms before setting up.

Does SWP affect the NAV of my fund?

No. SWP redeems your units at the prevailing NAV — it does not change the NAV itself, which is determined by the market value of the fund's portfolio. Your remaining units continue to reflect the same NAV as other investors in the same scheme.