What is IDCW in Mutual Funds?

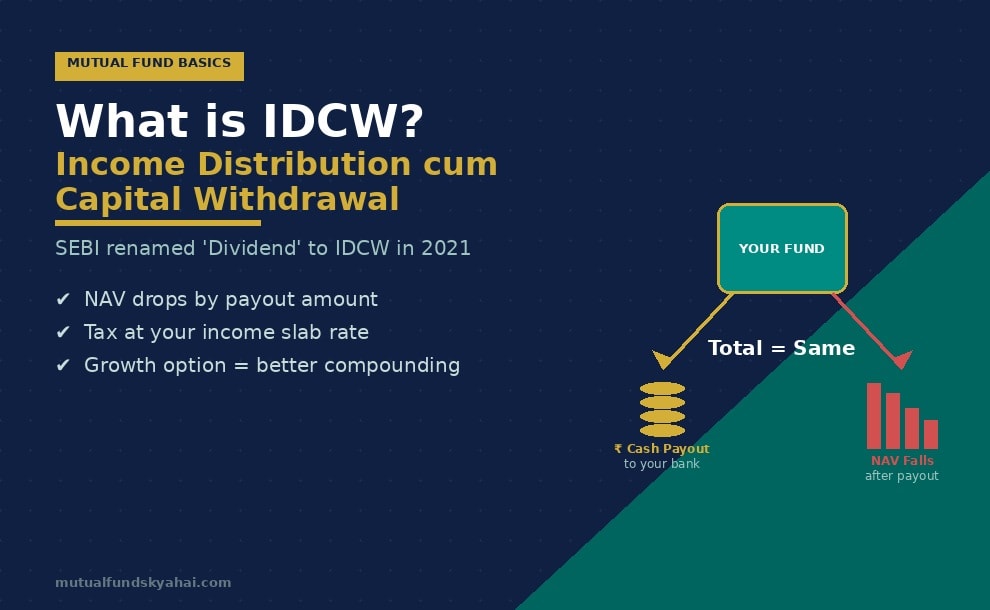

IDCW stands for Income Distribution cum Capital Withdrawal. It is the official name for what was previously called the "Dividend Option" in mutual funds. In April 2021, SEBI (Securities and Exchange Board of India) mandated that all mutual funds rename their Dividend option to IDCW — because the word "dividend" was misleading investors into thinking they were receiving a share of the fund's profits, similar to stock dividends.

In reality, a mutual fund payout under this option is not new income. It is a distribution made from the fund's existing Net Asset Value (NAV). When a payout is made, the NAV of the fund falls by exactly the amount distributed. In other words, you are partially withdrawing your own invested money — hence the name Income Distribution cum Capital Withdrawal.

How Does IDCW Work? A Simple Example

Let's say you hold 1,000 units of a mutual fund at an NAV of ₹50. Your total investment value is ₹50,000. The fund announces an IDCW payout of ₹3 per unit.

- You receive: 1,000 × ₹3 = ₹3,000 in your bank account

- The NAV falls from ₹50 to ₹47 after the payout

- Your remaining investment value: 1,000 × ₹47 = ₹47,000

- Total value (cash + investment): ₹3,000 + ₹47,000 = ₹50,000 — unchanged

The key insight is that your total wealth has not increased. You have simply converted part of your mutual fund investment into cash. No new income has been created. This is fundamentally different from a company dividend, where you receive a share of actual profits without your shareholding value falling.

Types of IDCW Payouts

1. Regular IDCW

Payouts are made at defined intervals — monthly, quarterly, or annually — depending on the scheme's design. These are common in debt funds like monthly income plans and conservative hybrid funds. However, these payouts are never guaranteed; the fund house pays IDCW only when there are distributable surpluses in the scheme and at the trustees' discretion.

2. Reinvestment IDCW

Instead of paying cash to your bank account, the IDCW amount is reinvested back into the same scheme at the prevailing NAV. This means you receive additional units rather than cash. The tax implications, however, remain the same as a regular IDCW payout — the reinvested amount is still treated as income in the hands of the investor at the time of distribution.

IDCW vs Growth Option — Which is Better?

This is one of the most frequently asked questions by Indian mutual fund investors. Here is a clear comparison:

- Growth Option: No payouts are made. All returns are reinvested within the scheme. The NAV keeps growing over time. You benefit from compounding and only pay capital gains tax when you actually redeem your units.

- IDCW Option: Payouts are made periodically. Each payout triggers a tax event. The NAV is reduced after every payout, limiting compounding. Cash flow is received regularly.

For long-term wealth creation, the Growth option is almost always superior because of two reasons: compounding is not interrupted by payouts, and you control when you realise gains (and therefore when you pay tax). The IDCW option may suit retirees or investors who need a steady cash flow from their investments — but even then, a Systematic Withdrawal Plan (SWP) on a Growth option fund is usually a more tax-efficient alternative.

Tax Treatment of IDCW in India

This is where IDCW becomes particularly important to understand. Prior to 2020, dividends from mutual funds were tax-free in the hands of the investor (the fund paid a Dividend Distribution Tax, or DDT). From 1 April 2020 onwards, this changed:

- IDCW payouts are now fully taxable as income in the hands of the investor, added to your total income and taxed at your applicable income tax slab rate.

- If your IDCW income in a financial year exceeds ₹5,000 from a single fund house, the AMC deducts TDS (Tax Deducted at Source) at 10% before crediting the payout to your account.

- This makes the IDCW option significantly less tax-efficient for investors in the 20% or 30% tax brackets compared to the Growth option, where Long Term Capital Gains (LTCG) tax at 12.5% applies after ₹1.25 lakh of gains per year.

Key Things to Watch Out For

- IDCW is not guaranteed income: Many investors in debt funds choose IDCW expecting regular monthly income. But payouts depend on distributable surplus and trustee approval — they can be reduced, skipped, or stopped at any time.

- NAV erosion is real: Every IDCW payout reduces the NAV by the payout amount. If you are not tracking this, it can feel like your investment is not growing — even when the fund is performing well.

- Reinvestment IDCW still triggers tax: Even if you opt for reinvestment (getting extra units instead of cash), the taxman treats it as income received, so you owe tax on it in that financial year.

- Don't confuse IDCW frequency with return: A fund paying monthly IDCW of ₹1/unit is not necessarily performing better than one paying ₹12/unit annually. Total return (NAV growth + distributions) is the correct measure.

- SWP is usually a smarter alternative: If you need regular cash flow, set up an SWP from a Growth option fund. You get the same periodic cash, but with better compounding and more tax-efficient treatment (you only pay capital gains tax on the gains portion of each withdrawal, not the full withdrawal amount).

Frequently Asked Questions

Why did SEBI rename Dividend to IDCW?

SEBI found that many investors — especially retail investors — were choosing the Dividend option under the mistaken belief that they were receiving extra profit from the fund, similar to company dividends. By renaming it IDCW and making the capital withdrawal nature explicit, SEBI aimed to improve transparency and investor awareness. The change was mandated in April 2021 and applies to all mutual fund schemes in India.

Is IDCW suitable for senior citizens who need regular income?

IDCW can provide periodic payouts, but the amounts are not fixed or guaranteed. A more reliable approach for senior citizens is to invest in a debt or conservative hybrid fund under the Growth option and set up a fixed monthly SWP. This provides predictable cash flow while keeping the corpus growing and managing tax efficiently.

What happens to my old Dividend option investments after the SEBI renaming?

Your existing investments in the Dividend option have been automatically renamed to IDCW — no action was required. The scheme's features, payout frequency, and your unit holdings remain exactly the same. Only the label has changed from "Dividend" to "IDCW".

Can I switch from IDCW to Growth option?

Yes. You can switch from the IDCW plan to the Growth plan of the same mutual fund scheme. However, this switch is treated as a redemption and fresh purchase for tax purposes — so you may need to pay capital gains tax on any gains made until the switch date. Consult your financial advisor before making this move, especially if you hold equity funds where LTCG tax applies.

The Bottom Line

IDCW is a renamed and rebranded version of the old Dividend option in mutual funds — but the name change also carries an important message. Every IDCW payout is a withdrawal from your own capital, not a bonus. For most investors focused on long-term wealth creation, the Growth option combined with an SWP is a superior strategy — offering better compounding, more control, and greater tax efficiency.

Understanding IDCW is an important step in making smarter mutual fund choices. For more plain-language guides on mutual fund concepts, explore mutualfundskyahai.com.