What is Duration Risk in Debt Mutual Funds?

Duration risk — also called interest rate risk — is the risk that a debt mutual fund's NAV will fall when interest rates rise. It is one of the most important but least understood risks for investors in debt funds, and understanding it can help you choose the right debt fund for your time horizon and market view.

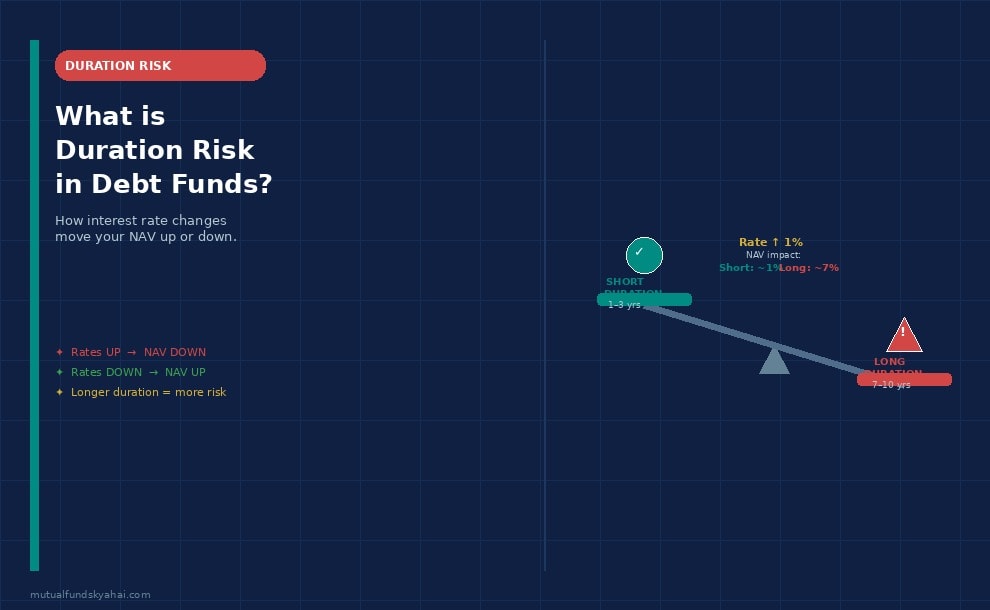

In simple terms: when market interest rates go up, the price of existing bonds falls — and when rates fall, bond prices rise. A debt mutual fund holds a portfolio of bonds, so its NAV moves in the opposite direction of interest rates. The longer the maturity of the bonds a fund holds, the more sensitive its NAV is to interest rate movements. This sensitivity is measured by a concept called duration.

How Does Duration Risk Work?

To understand duration risk, it helps to first understand why bond prices and interest rates move in opposite directions.

Suppose you hold a 10-year government bond paying a fixed coupon of 7% per year. If market interest rates rise to 8%, newly issued bonds now pay 8%. Your old bond paying only 7% becomes less attractive — so its market price falls until its effective yield matches the new 8% rate. Conversely, if rates fall to 6%, your 7% bond becomes more valuable and its price rises.

This inverse relationship is the core of duration risk. The key measure is Modified Duration, which tells you approximately how much a fund's NAV will change for every 1% change in interest rates:

- A fund with a modified duration of 5 years: if interest rates rise by 1%, the fund's NAV will fall by approximately 5%.

- A fund with a modified duration of 1 year: the same 1% rate rise causes only a 1% NAV drop.

Example: You invest ₹1 lakh in a gilt fund with a modified duration of 7 years. The RBI unexpectedly raises the repo rate by 0.5%. Your fund's NAV would fall by approximately 3.5% (7 × 0.5), reducing your investment value to roughly ₹96,500 in the short term.

Types of Duration in Debt Funds

You will encounter two related but distinct terms when evaluating debt funds:

- Macaulay Duration: The weighted average time (in years) to receive all the cash flows from a bond — coupons plus principal repayment. Think of it as the "effective maturity" of a bond or portfolio. A longer Macaulay duration means more of the bond's value is tied up in distant cash flows, making it more sensitive to rate changes.

- Modified Duration: Derived from Macaulay Duration, this is the practical measure used to estimate NAV sensitivity. Modified Duration = Macaulay Duration ÷ (1 + yield). Fund factsheets and SEBI disclosures typically report modified duration.

SEBI requires all debt mutual funds in India to disclose their portfolio's modified duration in their monthly factsheets, making it easy to compare funds.

Duration Risk Across Different Debt Fund Categories

SEBI categorises debt funds partly based on their duration and maturity profiles. Here is how duration risk varies across categories:

- Overnight and Liquid Funds — Duration of less than 1 day to 91 days. Negligible duration risk. Suitable for parking short-term money.

- Ultra Short Term and Low Duration Funds — Duration of 3 to 12 months. Very low sensitivity to rate changes.

- Short Duration and Banking & PSU Funds — Duration of 1 to 3 years. Moderate rate sensitivity.

- Medium Duration and Corporate Bond Funds — Duration of 3 to 4+ years. Higher sensitivity; better suited to stable or falling rate environments.

- Long Duration and Gilt Funds — Duration of 7+ years. Highest sensitivity to interest rate changes. Can deliver strong returns when rates fall but can suffer sharp NAV cuts when rates rise.

- Dynamic Bond Funds — Duration can vary significantly (1 to 10+ years) as the fund manager actively adjusts based on the interest rate outlook.

Who Should Be Concerned About Duration Risk?

- Short-term investors (less than 1 year): Stick to overnight, liquid, or ultra short-term funds with very low duration. You have little time to recover from an unexpected NAV dip caused by rate hikes.

- Medium-term investors (1–3 years): Short-duration or banking & PSU funds are appropriate. Moderate duration means manageable rate sensitivity.

- Long-term investors (3+ years) who believe rates will fall: Medium or long duration funds can reward you handsomely as falling rates push up NAVs. But you need conviction and patience.

- Risk-averse investors: Prefer funds with low modified duration regardless of the market cycle. Avoid gilt and long-duration funds unless you specifically want interest rate exposure.

Key Things to Watch Out For

- Check modified duration before investing: Every debt fund's factsheet discloses modified duration. As a rule of thumb, match the fund's duration to your investment horizon. A 5-year duration fund is not appropriate for a 1-year goal.

- Duration risk compounds with credit risk: A long-duration fund holding lower-rated bonds faces both interest rate risk and credit risk simultaneously. Gilt funds (which hold only government securities) carry duration risk but zero credit risk — the trade-off is explicit.

- Rate cycles matter: In a rising rate environment, short-duration funds protect capital. In a falling rate environment, long-duration funds amplify gains. Timing this cycle is difficult — most retail investors are better off staying in the duration range matching their horizon.

- Yield to Maturity (YTM) vs NAV movement: Duration risk affects the short-term NAV. But if you hold a fund long enough (beyond its duration), you tend to earn close to the YTM declared at the time of investment. Duration risk is most painful for those who exit at the wrong time.

- Do not confuse maturity with duration: A 10-year bond paying semi-annual coupons has a Macaulay duration of roughly 7–8 years, not 10 years, because some cash flows arrive earlier. Zero-coupon bonds have duration equal to their maturity.

Frequently Asked Questions

Is duration risk the same as credit risk?

No. Duration risk (interest rate risk) is the risk of NAV falling due to rising interest rates — it affects even the safest government bond funds. Credit risk is the risk of a bond issuer defaulting or being downgraded. A fund can have high duration risk with zero credit risk (e.g., a gilt fund) or low duration risk with significant credit risk (e.g., a short-maturity credit risk fund).

How can I find a debt fund's modified duration?

SEBI mandates disclosure of modified duration in every debt fund's monthly portfolio statement and factsheet. You can find this on the AMC's website, on platforms like MFI Explorer or Value Research, or in the fund's monthly factsheet PDF. Compare modified duration across similar funds before investing.

If a debt fund's NAV falls due to rising rates, should I redeem?

Not necessarily. If your investment horizon is longer than the fund's duration, the NAV dip is likely temporary. As the bonds in the portfolio mature and are reinvested at higher yields, the fund's returns tend to recover. Redemption during a rate-driven dip locks in your loss. Assess whether your original investment thesis still holds before deciding.

What happened to long-duration debt funds in India during rate hike cycles?

During the RBI rate hike cycles of 2018 and 2022–23, long-duration and gilt funds delivered negative or flat returns over 6–12 month periods as yields rose sharply. Investors who stayed invested for 2–3 years subsequently recovered and earned positive returns. This illustrates why duration alignment with your horizon matters more than chasing the highest yielding debt fund.