Can Indian Investors Buy US Stocks Through Mutual Funds?

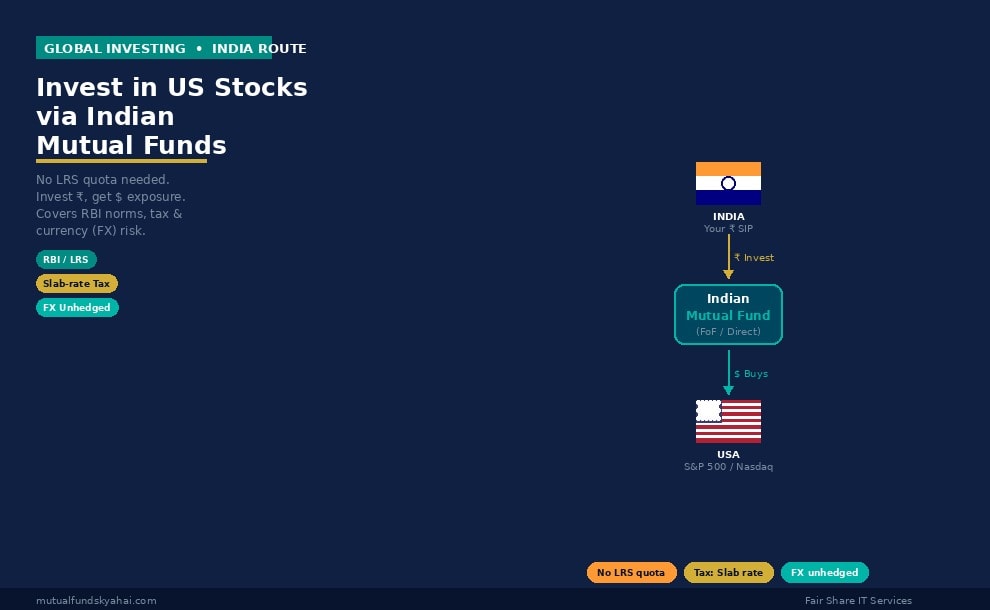

Yes — Indian retail investors can gain exposure to US stocks such as Apple, Microsoft, Amazon, and the S&P 500 index without opening a foreign brokerage account. The simplest route is through Indian mutual funds that invest in overseas markets, either directly or via a feeder fund structure. This is legal, regulated, and available to any KYC-compliant investor in India with a PAN card and a bank account.

However, this route comes with important regulatory guardrails, tax implications, and currency risks that every investor must understand before committing money.

How the Indian Mutual Fund Route to US Markets Works

There are two common structures through which Indian AMCs offer US market exposure:

1. Fund of Funds (FoF) investing in overseas funds

An Indian AMC launches a Fund of Funds that collects rupee investments from Indian investors and uses the corpus to purchase units of an existing overseas fund — typically a US-domiciled ETF or a UCITS fund tracking the S&P 500, Nasdaq 100, or a thematic index. Examples include Motilal Oswal Nasdaq 100 FoF, Mirae Asset NYSE FANG+ ETF FoF, and Franklin India Feeder — Franklin US Opportunities Fund.

2. Direct overseas equity funds

Some Indian AMCs manage funds that directly purchase overseas listed stocks — for instance, buying shares of Google, Meta, or Tesla from their Indian fund corpus. These funds require SEBI approval and are subject to the industry-wide overseas investment limit.

In both structures, you invest in Indian rupees, and the fund handles the currency conversion, overseas remittance, and foreign asset custody. From your perspective, the process is identical to investing in any domestic mutual fund — SIP, lump sum, or direct plan on any MF platform.

The SEBI Overseas Investment Limit: Why Some Funds Are Paused

This is the most important regulatory constraint to understand. SEBI imposes an industry-wide limit on how much Indian mutual funds can collectively invest overseas. As of the most recent SEBI directive, the aggregate overseas investment limit for all Indian mutual funds combined is USD 7 billion, with an additional USD 1 billion sub-limit for overseas ETFs.

This limit was breached in early 2022 — after a surge of inflows into international funds — and SEBI directed all AMCs to stop accepting fresh subscriptions (including new SIPs) in overseas funds. Many popular US equity mutual funds in India remain paused for new lump-sum investments as of the time of writing, though some AMCs have opened windows for small SIP amounts as their corpus dips below the threshold.

What this means for you: Before trying to invest in a US-focused fund, check whether that specific fund is currently accepting subscriptions. The AMC's website or your MF platform will clearly indicate "Temporarily Suspended" or "Paused" if fresh investments are not allowed. Existing investors can continue SIPs and redemptions unaffected.

RBI Norms: The Liberalised Remittance Scheme (LRS)

When an Indian mutual fund remits money overseas to buy US stocks, it does so under the Reserve Bank of India's Liberalised Remittance Scheme (LRS). However, individual investors investing via an Indian mutual fund do not need to use their own LRS limit — the remittance is done by the AMC as an institutional remittance, not by you personally.

Your personal LRS limit of USD 250,000 per financial year applies only if you invest directly in foreign markets — for example, through a platform like Vested, INDmoney, or an overseas brokerage account. When you invest through an Indian mutual fund, the AMC manages the overseas remittance on behalf of all unitholders collectively, and your LRS quota is not consumed.

One important note: TCS (Tax Collected at Source) at 20% applies on LRS remittances above ₹7 lakh per financial year (as per Finance Act 2023 amendments). Again, this applies to direct personal remittances, not to investments through Indian mutual funds. Investing via an Indian FoF or overseas fund is therefore also more convenient from a TCS compliance standpoint.

Income Tax Treatment: What You Owe the Government

This is where international mutual funds differ significantly from domestic equity funds. The tax treatment depends on how SEBI classifies the fund:

Fund of Funds and Overseas Equity Funds: Taxed as Debt Funds

Even though a US equity FoF invests in stocks of Apple, Google, and other companies, SEBI and the Income Tax Act classify it as a non-equity fund for tax purposes — because less than 65% of its assets are in Indian equities. This means:

- Capital gains (short-term or long-term) are taxed at your income tax slab rate, regardless of holding period.

- There is no LTCG exemption of ₹1.25 lakh as available for equity funds.

- There is no benefit of the flat 12.5% LTCG rate applicable to equity funds after 1 year.

- Gains are added to your total income and taxed at 5%, 20%, or 30% depending on your slab.

This is a significant disadvantage compared to domestic equity mutual funds. A 30% taxpayer holding a US FoF for 5 years will pay 30% tax on gains — compared to 12.5% LTCG for a domestic equity fund held for over 1 year.

Note: The earlier indexation benefit for long-term debt/FoF gains (available for investments made before April 1, 2023) has been removed for new investments. Consult a tax advisor for the treatment of pre-April 2023 investments.

Dividend/IDCW Payouts

Any dividends distributed by a US equity FoF are added to your income and taxed at slab rate. TDS at 10% is deducted if the annual payout exceeds ₹5,000. Choosing the Growth option (as with all mutual funds) avoids this annual tax drag.

Currency Risk: How the Rupee-Dollar Rate Affects Your Returns

When you invest in a US equity fund via an Indian mutual fund, your returns have two components: the performance of US stocks in USD and the movement of the INR/USD exchange rate.

Historically, the Indian rupee has depreciated against the US dollar at roughly 3–5% per year on average. This depreciation works in favour of the Indian investor — if the S&P 500 returns 10% in USD terms and the rupee depreciates by 4%, your INR return is approximately 14.4% (10% × 1.04 currency gain).

However, this is not always the case. If the rupee appreciates — as it occasionally does in short bursts — the currency movement reduces your returns. For example, if the S&P 500 returns 8% in USD but the rupee strengthens by 3%, your INR return is only about 4.8%.

Key points on FX risk:

- Indian FoFs that invest in US funds do not typically hedge the currency exposure. You get full, unhedged currency risk.

- Over the long term (10+ years), rupee depreciation has historically enhanced returns for Indian investors in US funds.

- In the short term (1–3 years), currency movements can be volatile and unpredictable, adding to NAV volatility beyond what the underlying US index itself shows.

- If the rupee moves sharply in either direction (e.g., RBI intervention, global risk-off events), your fund's NAV can move significantly even on days when US markets are closed.

Who Should Consider Investing in US Stocks via Indian Mutual Funds?

- Long-term investors (7+ years): The compounding of US corporate earnings, rupee depreciation tailwind, and diversification benefits are most visible over long horizons.

- Investors seeking geographic diversification: Indian equities can be highly correlated with domestic macro cycles. Adding US exposure reduces country-specific risk in a portfolio.

- Tech-oriented investors: India's market has limited exposure to global technology giants. A Nasdaq 100 or FANG+ fund gives direct access to the world's largest technology companies.

- Investors comfortable with higher tax: Given the slab-rate taxation, this route makes most financial sense for investors in the 5–20% tax bracket or those holding for very long periods where compounding outweighs the tax disadvantage.

Key Things to Watch Out For

- Check if the fund is open for subscriptions: Due to the SEBI overseas limit cap, many funds remain paused. Always verify before investing.

- Understand the TER stack: A FoF charges its own expense ratio on top of the underlying overseas fund's expense ratio. The all-in cost can be 1.5–2.5% per year — higher than a direct domestic equity fund.

- Do not time currency: Most retail investors cannot reliably predict INR/USD movements. Invest via SIP to average out both market and currency fluctuations over time.

- Keep tax implications in mind at redemption: Entire gains are taxed at slab rate. Plan large redemptions across financial years if possible to manage tax outflow.

- Tracking error in FoF structure: A FoF that invests in an ETF has a two-layer structure — the Indian fund tracking the overseas ETF, and the ETF tracking the index. Both can have tracking error, slightly reducing returns versus the benchmark index.

Frequently Asked Questions

Do I need to report US mutual fund investments in my ITR?

If you hold units of an Indian mutual fund (even one that invests overseas), you are holding an Indian mutual fund unit — not a foreign asset. You do not need to report it under Schedule FA (Foreign Assets) in your ITR. However, any capital gains on redemption must be reported under the appropriate capital gains schedule.

What is the difference between a Nasdaq 100 Index Fund and a Nasdaq 100 FoF?

A Nasdaq 100 Index Fund directly replicates the Nasdaq 100 index by buying individual stocks. A Nasdaq 100 FoF invests in an overseas ETF that tracks the Nasdaq 100 — adding a layer of structure and cost. Both are taxed identically as non-equity funds. Index funds may have slightly lower TER and better tracking accuracy if managed well.

Can I do an SIP in a US equity fund?

Yes, if the fund is currently open for subscriptions. Many AMCs allow SIPs of ₹500–₹1,000 per month in their international fund offerings when fresh subscription windows are available. Check the current status on the AMC's website or your investment platform.

Is it better to invest directly in US stocks via LRS or through an Indian mutual fund?

Both routes have trade-offs. Direct investing via LRS (using platforms like Vested or INDmoney) gives you lower cost and direct stock selection, but consumes your LRS quota and requires self-managed tax filing. The Indian mutual fund route is simpler, does not consume your LRS quota, and consolidates all reporting in your Indian MF statement — but carries higher costs and less favourable taxation compared to direct equity gains abroad.