What is Credit Risk in Debt Mutual Funds?

Credit risk — also called default risk — is the possibility that a bond issuer (a company, NBFC, or government entity) may fail to pay back the interest or principal on its debt on time, or at all. When a debt mutual fund holds such bonds in its portfolio and the issuer defaults or gets its credit rating downgraded, the fund's NAV drops — sometimes sharply and suddenly.

Unlike interest rate risk, which affects all debt funds when market yields move, credit risk is specific to individual issuers. A debt fund that holds high-quality AAA-rated bonds has very low credit risk. A fund that chases higher yields by holding lower-rated or unrated bonds carries significant credit risk — and potentially much higher rewards in normal times, but devastating losses when things go wrong.

In India, credit risk in mutual funds became a front-page issue during the IL&FS crisis (2018), the DHFL default (2019), and the Vodafone Idea write-down saga — events that caused sharp NAV drops in several debt funds overnight and left investors shocked.

How Credit Ratings Work in India

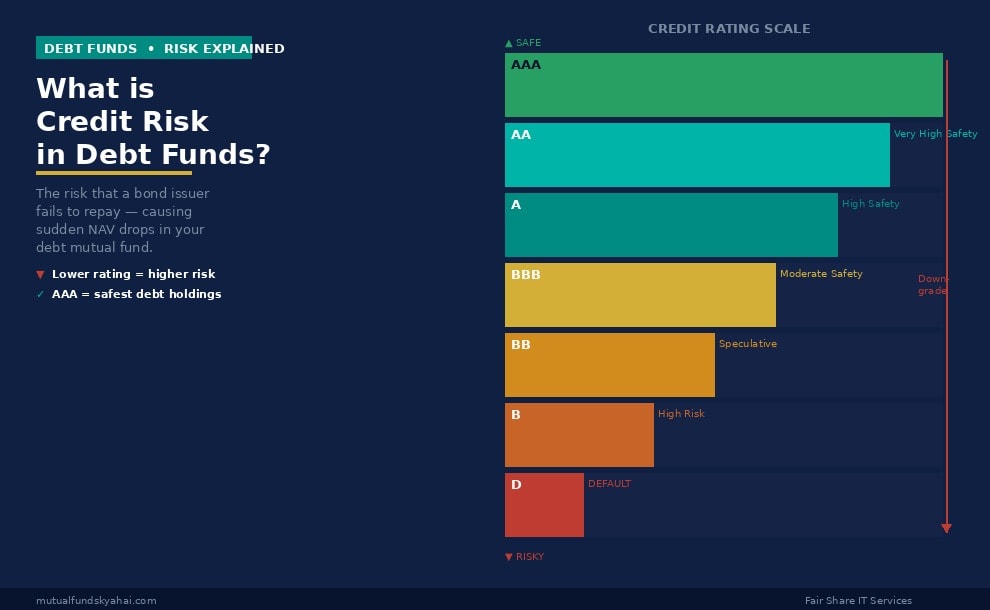

Credit rating agencies — CRISIL, ICRA, CARE Ratings, and India Ratings — assess the creditworthiness of bond issuers and assign ratings that indicate the likelihood of timely repayment. The rating scale works as follows:

- AAA: Highest safety. Extremely low credit risk. Typically assigned to large, financially strong companies and government-backed entities.

- AA: Very high safety. Marginally higher risk than AAA, but still considered investment-grade.

- A: High safety. Adequate capacity to meet financial obligations.

- BBB: Moderate safety. Considered the lowest investment-grade rating.

- BB and below: Speculative or "junk" grade. Significant credit risk. Higher yields offered to compensate investors.

- D: Default. The issuer has already missed a payment.

Ratings can be further qualified with "+" or "−" suffixes (e.g., AA+ or AA−) to indicate relative standing within a category. SEBI requires debt mutual funds to mark down the NAV of a bond when its rating is downgraded below investment grade, and write it off if it defaults — which is what causes the sudden NAV drops investors sometimes experience.

How Credit Risk Affects a Debt Fund's NAV

Suppose a debt fund holds bonds issued by a large NBFC with an AA rating. The bonds are priced at par (₹100 face value). Now, suppose the NBFC faces a liquidity crisis and is downgraded to BBB. The market price of those bonds immediately falls — say to ₹85 — as investors demand higher yields to compensate for the increased risk. The fund's NAV falls in proportion to how much of the portfolio this issuer represents.

If the NBFC then defaults entirely, the bonds may be written down to ₹0, causing a catastrophic NAV fall. Investors who redeem after such a write-down suffer the full loss.

Real example: In 2019, when DHFL defaulted on its commercial paper, several debt funds that held DHFL paper saw their NAVs fall by 5–53% in a single day, depending on their exposure. Investors who had parked money in these funds for "safety" suffered severe capital losses.

Types of Debt Funds by Credit Risk

SEBI classifies debt funds partly based on the credit quality of their holdings:

- Overnight and Liquid Funds: Hold only the safest, shortest-maturity instruments. Virtually zero credit risk.

- Banking and PSU Funds: Invest in bonds issued by banks and public sector undertakings — generally AA+ or AAA rated. Low credit risk.

- Corporate Bond Funds: Must invest at least 80% in AA+ or above rated bonds. Low-to-moderate credit risk.

- Short Duration / Medium Duration Funds: May hold a mix of ratings. Credit quality varies by fund house.

- Credit Risk Funds: SEBI-defined category that must invest at least 65% in below AA-rated bonds. These are specifically designed to take on credit risk for higher yield — and carry the highest default risk.

Who Should Be Careful About Credit Risk?

- Conservative investors: If capital preservation is your primary goal, stay with liquid funds, overnight funds, or banking & PSU funds — all of which carry negligible credit risk.

- Investors using debt funds as an FD substitute: Many retail investors park short-term money in debt funds assuming they are as safe as FDs. This is not always true — especially for funds with lower-rated holdings.

- Credit risk fund investors: These funds explicitly hold lower-rated bonds. They can generate 1–2% higher returns than AAA funds in normal times, but a single major default in the portfolio can wipe out years of extra returns.

- Retirees and near-retirees: Those dependent on their corpus for income should avoid credit risk entirely. A 10–20% NAV drop at retirement is extremely difficult to recover from.

Key Things to Watch Out For

- Check the portfolio's credit quality: Before investing in any debt fund, review the credit rating breakdown in the monthly factsheet. Prefer funds with 80%+ in AAA or equivalent (like G-secs and T-Bills).

- Concentration risk: A fund holding 15–20% in a single issuer amplifies the damage if that issuer defaults. SEBI limits single-issuer exposure to 10% of AUM, but check the actual portfolio.

- Do not chase yield: If a debt fund is offering 9–10% returns while peers offer 7%, it is almost certainly taking on higher credit risk. Higher yield = higher risk is a universal rule in fixed income.

- Rating upgrades and downgrades happen fast: A bond can go from AA to junk in weeks during a crisis. No fund manager can always predict this. Diversification across issuers and regular portfolio reviews by the AMC are your best protection.

- Segregated portfolios (Side-pocketing): SEBI introduced side-pocketing rules in 2018, allowing fund houses to segregate defaulted bonds from the main portfolio so that existing investors bear the loss and new investors are not affected. If you see a "segregated portfolio" NAV on your statement, that portion has defaulted.

Frequently Asked Questions

Are government bond funds (gilt funds) completely free of credit risk?

Yes — gilt funds that invest only in central government securities carry zero credit risk, since the Government of India cannot default on domestic currency obligations. However, gilt funds carry high interest rate risk. So while credit risk is absent, market risk (NAV volatility) is present.

How can I check the credit quality of a debt fund before investing?

Look at the fund's latest monthly factsheet (available on the AMC's website or AMFI). It shows a breakdown of the portfolio by rating category — e.g., "AAA: 78%, AA: 15%, A: 7%." You can also check Value Research or Morningstar India for a portfolio credit quality summary.

Is a credit risk fund always a bad investment?

Not necessarily. Credit risk funds can deliver superior returns over long periods (5+ years) if the fund manager is skilled at identifying fundamentally sound but temporarily undervalued issuers. However, they require a long investment horizon, high risk tolerance, and conviction in the fund house's credit research capability. They are not suitable for short-term or conservative investors.

What happens to my money if a debt fund's holding defaults?

The fund marks down (or writes off) the defaulted bond's value in the portfolio. The NAV falls by the proportional impact of the write-down. If SEBI's side-pocketing rules are triggered, the defaulted portion is moved to a separate NAV. You continue to hold units in the main fund at the adjusted NAV, and the segregated portion may recover value if the issuer eventually repays — but this can take years, and full recovery is not guaranteed.