What is Asset Allocation?

Asset allocation is the process of dividing your investment portfolio across different asset classes — such as equity, debt, gold, and cash — based on your financial goals, investment horizon, and risk tolerance. It is widely considered the single most important decision in investing, as research consistently shows that asset allocation explains the majority of a portfolio's long-term returns and volatility.

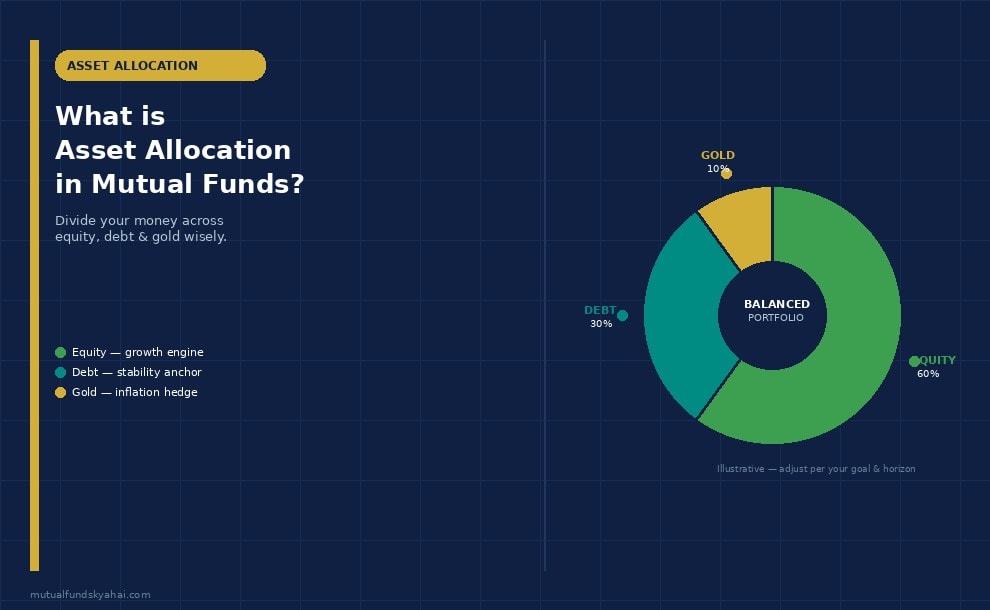

In the context of mutual funds, asset allocation means deciding how much of your money to put in equity funds (stocks), debt funds (bonds), and other categories like gold funds or international funds. Getting this mix right — and rebalancing it over time — is the foundation of sound financial planning.

Why Does Asset Allocation Matter?

Different asset classes behave differently in varying market conditions:

- Equity offers higher long-term growth but is volatile in the short term. It tends to outperform in bull markets but can fall sharply during economic downturns.

- Debt provides stability and regular income. It typically holds its value or grows modestly even when equity markets fall, acting as a cushion.

- Gold often rises during periods of inflation, currency weakness, or geopolitical uncertainty — making it a useful diversifier.

By spreading investments across these classes, asset allocation reduces the impact of any single asset class performing poorly. A portfolio that is 100% in equity would have suffered a 50%+ drawdown during the 2008 financial crisis. A balanced 60% equity / 40% debt portfolio would have fallen much less and recovered faster.

How Does Asset Allocation Work in Practice?

Asset allocation follows a simple process:

- Step 1 — Define your goal and horizon: Are you saving for retirement in 25 years, a child's education in 10 years, or a house down payment in 3 years? Longer horizons allow more equity exposure; shorter ones require more stability.

- Step 2 — Assess your risk tolerance: How would you react if your portfolio dropped 30% in a year? If you would panic and sell, a heavy equity allocation is not right for you regardless of your horizon.

- Step 3 — Set your target allocation: Based on goals and risk, decide your equity-debt-gold split. Common frameworks are described below.

- Step 4 — Choose funds accordingly: Select mutual funds within each asset class that match your quality and cost criteria.

- Step 5 — Rebalance periodically: As markets move, your actual allocation drifts from your target. Rebalancing (typically once a year) brings it back in line.

Common Asset Allocation Frameworks

Several rule-of-thumb frameworks exist to help investors determine their equity allocation:

- The 100-minus-age rule: Your equity allocation (%) = 100 minus your age. A 30-year-old would hold 70% in equity. This is a starting point, not a rigid rule — many financial planners now use 110 or 120 minus age given longer life expectancies.

- Conservative (20-80): 20% equity, 80% debt. Suitable for retirees, very risk-averse investors, or those with short horizons (less than 2 years).

- Moderate (50-50): 50% equity, 50% debt. A classic balanced approach for medium-term goals (3–7 years) or moderate risk tolerance.

- Aggressive (80-20): 80% equity, 20% debt. Suitable for young investors with long horizons (10+ years) and high risk tolerance.

- All-equity (100% equity): Only appropriate for investors with very long horizons (15+ years), high risk tolerance, and the discipline not to panic-sell during corrections.

Adding 5–10% in gold can improve diversification for any of the above allocations, particularly as a hedge against inflation and currency risk.

Asset Allocation Through Mutual Fund Categories

SEBI's mutual fund categorisation makes it easy to implement an asset allocation strategy:

- Equity component: Large cap, flexi cap, multi cap, or index funds for the core; mid/small cap funds for higher growth potential.

- Debt component: Short-duration, banking & PSU, or corporate bond funds for stability; liquid funds for emergency reserves.

- Gold component: Gold ETFs or Gold Fund of Funds (no physical gold storage required).

- Hybrid funds as a shortcut: Aggressive Hybrid Funds (65–80% equity), Balanced Advantage Funds (dynamic equity allocation), and Conservative Hybrid Funds (25–40% equity) each maintain a target allocation internally, making them a single-fund solution for many investors.

Who Should Think About Asset Allocation?

- Young investors (20s–30s): Can afford a higher equity allocation (70–100%) given the long runway to recover from market dips.

- Mid-career investors (40s): Should begin gradually shifting towards a more balanced allocation (50–70% equity) as retirement approaches.

- Pre-retirees and retirees (55+): Capital preservation becomes a priority — a lower equity allocation (20–40%) with a focus on income-generating debt funds is typically appropriate.

- Goal-based investors: Each financial goal should have its own asset allocation based on its timeline. A long-term goal (retirement) can be equity-heavy while a near-term goal (buying a car in 2 years) should be entirely in debt.

Key Things to Watch Out For

- Do not ignore rebalancing: After a strong equity rally, your 60-40 portfolio may drift to 75-25. Without rebalancing, you take on more risk than intended. Set a calendar reminder to review and rebalance once a year, or whenever an asset class deviates more than 5–10% from its target.

- Avoid over-diversification: Holding 15 equity funds does not improve diversification — many of them will own the same stocks. A well-chosen set of 3–5 funds across large, mid, and small cap categories is typically sufficient.

- Account for all assets, not just mutual funds: Your EPF, PPF, real estate, and FDs are also part of your asset allocation picture. If you already have substantial debt exposure through EPF and PPF, you may not need additional debt mutual funds.

- Do not confuse diversification with asset allocation: Diversification means spreading within an asset class (holding many stocks). Asset allocation is the higher-level decision of how to split across asset classes. Both matter.

- Taxation affects net returns: Equity funds held over 1 year attract 12.5% LTCG tax on gains above ₹1.25 lakh. Debt fund gains are taxed at your income slab rate. Factor this into your allocation decision, especially in higher tax brackets.

Frequently Asked Questions

Is there a "perfect" asset allocation?

No. The ideal allocation is deeply personal and depends on your goals, time horizon, income stability, risk tolerance, and existing assets. Two investors of the same age with different risk appetites and goals may need very different allocations. What matters most is that your allocation lets you stay invested through market volatility without panic-selling.

Should I change my asset allocation when markets are high or low?

Generally, no — trying to time the market by shifting allocation based on valuations is difficult and often backfires. Rebalancing (returning to your target allocation when it drifts) is different from market timing and is perfectly appropriate. Some investors use valuation-based dynamic allocation (as done by Balanced Advantage Funds), but this requires discipline and a clear process.

What is a Balanced Advantage Fund and how does it relate to asset allocation?

A Balanced Advantage Fund (BAF) dynamically shifts its equity-debt allocation based on market valuations — typically increasing equity when markets are cheap and reducing it when expensive. The fund manager handles the asset allocation decision for you. This makes BAFs a useful option for investors who want a hands-off approach to managing equity-debt balance.

How often should I review my asset allocation?

A full review once a year is generally sufficient for most investors. You should also review when a major life event occurs — marriage, birth of a child, job change, inheritance — or when you are within 2–3 years of a financial goal. At that point, gradually shifting from equity to debt helps protect the accumulated corpus from a last-minute market correction.