What is a Multi Cap Fund?

A Multi Cap Fund is an open-ended diversified equity mutual fund that invests across large cap, mid cap, and small cap companies with a mandatory minimum allocation of 25% each to all three segments. This SEBI-mandated 25-25-25 rule is what makes Multi Cap funds distinctively different from other diversified equity categories. With 75% locked into the three-way split, the fund manager has discretion over the remaining 25%, which can be allocated to any segment. The fund must maintain at least 75% in equity at all times.

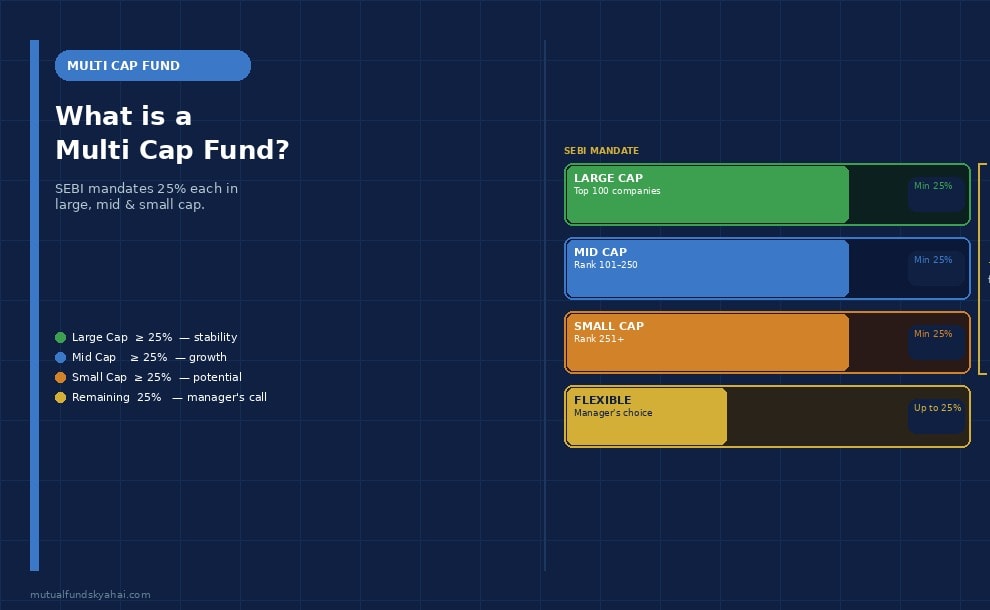

The SEBI 25-25-25 Rule Explained

Before September 2020, funds marketed as "Multi Cap" had no fixed allocation requirement. Most fund managers, preferring the stability of large caps, ended up running portfolios that were 70–80% large cap. Retail investors expecting meaningful mid and small cap exposure were often surprised to find they had essentially bought a large cap fund with a different label.

In September 2020, SEBI mandated the following minimum allocations:

- Large Cap (Top 100 companies): Minimum 25%

- Mid Cap (Companies ranked 101–250): Minimum 25%

- Small Cap (Companies ranked 251+): Minimum 25%

The remaining 25% can go anywhere at the fund manager's discretion. This rule ensures investors genuinely get exposure to all three segments.

How Does a Multi Cap Fund Work in Practice?

Consider a Multi Cap fund with ₹1,000 crore in assets. Under SEBI's rules, it must hold at least ₹250 crore each in large, mid, and small cap stocks. The remaining ₹250 crore can go anywhere. A typical portfolio might look like 35% large cap, 35% mid cap, 30% small cap — giving balanced exposure across the spectrum while the fund manager adds value through stock selection within each segment. The mandatory 25% small cap allocation is the most distinctive characteristic, forcing exposure to high-growth but volatile small cap companies that large-cap-heavy funds often under-represent.

Multi Cap vs Flexi Cap — Key Differences

- Allocation flexibility: Multi Cap must maintain at least 25% in each segment. Flexi Cap has no minimum in any segment — the manager decides freely.

- Small cap guarantee: Multi Cap guarantees at least 25% in small caps. Flexi Cap managers often hold very little small cap in volatile markets.

- Risk profile: Multi Cap tends to be more volatile due to the mandatory small cap floor. Flexi Cap can be more conservative when managers reduce mid/small cap exposure.

- Manager dependency: Flexi Cap returns depend heavily on allocation calls. Multi Cap returns depend more on stock selection within each fixed segment.

Who Should Invest in a Multi Cap Fund?

- Investors wanting guaranteed diversification: Multi Cap delivers structured exposure to all three market cap segments by regulatory mandate — not just marketing.

- Long-term investors (7+ years): The mandatory 25% small cap minimum means significant volatility. You need a long runway to ride out mid and small cap drawdowns.

- Investors comfortable with higher volatility for higher potential returns: Mid and small cap stocks have historically outperformed large caps over long periods in India, but with considerably more volatility.

- Investors who want simplicity: A single Multi Cap fund gives structured exposure to the full equity market without managing multiple cap-specific funds separately.

Key Things to Watch Out For

- Higher volatility than large cap funds: The mandatory 25% small cap floor means Multi Cap funds can fall sharply during corrections. Ensure your time horizon is long enough to absorb this.

- Liquidity risk in small caps: Small cap stocks are less liquid. In a sharp downturn, meeting redemptions by selling small cap positions can be challenging — making Multi Cap unsuitable for short-term goals.

- Benchmark: Use the Nifty 500 Multicap 50:25:25 Index as the benchmark for Multi Cap funds, not the Nifty 50 or plain Nifty 500.

- Expense ratio: Active Multi Cap funds typically carry expense ratios of 1.5–2.0% for regular plans and 0.5–1.0% for direct plans. The lower the expense ratio, the better your net return over time.

- Taxation: Equity fund rules apply. Long-term capital gains (held over 1 year) above ₹1.25 lakh are taxed at 12.5%. Short-term gains are taxed at 20%.

Frequently Asked Questions

Why did SEBI create the 25-25-25 rule?

To ensure genuine diversification and protect investors from misleading fund labelling. Before 2020, most "Multi Cap" funds were effectively large cap funds. The rule forces meaningful capital allocation to mid and small cap companies. Fund managers who preferred an unconstrained mandate were given the option to convert their funds to the newly created Flexi Cap category.

Are Multi Cap funds riskier than large cap funds?

Yes, generally. The mandatory 25% in small caps adds meaningful volatility that pure large cap funds do not carry. Over a long horizon, this risk has historically been rewarded with higher returns. Over short periods, Multi Cap funds can significantly underperform large cap funds when small and mid caps sell off.

What is the difference between Multi Cap and Aggressive Hybrid funds?

Multi Cap funds are 100% equity across market caps. Aggressive Hybrid funds hold 65–80% in equity and 20–35% in debt. The debt component makes Aggressive Hybrid funds less volatile and more suitable for moderate-risk investors, while Multi Cap funds are a pure equity play across the full market cap spectrum.

How many Multi Cap funds should I hold?

One is typically sufficient as a diversified equity core. If you already hold a Flexi Cap fund, adding a Multi Cap brings guaranteed mid and small cap exposure your Flexi Cap may not provide. Avoid holding more than one Multi Cap fund — the stock overlap across funds would be significant.