What Is the Dividend Option vs Growth Option in Mutual Funds?

When you invest in a mutual fund in India, you are typically asked to choose between two plans: the Growth Option and the Dividend Option (now officially renamed IDCW — Income Distribution cum Capital Withdrawal by SEBI). Both options invest in the same underlying portfolio of stocks or bonds, but they differ in how they handle the profits generated by the fund.

Understanding this difference is crucial because it affects your returns, tax liability, and cash flow — especially over the long term.

How Does the Growth Option Work?

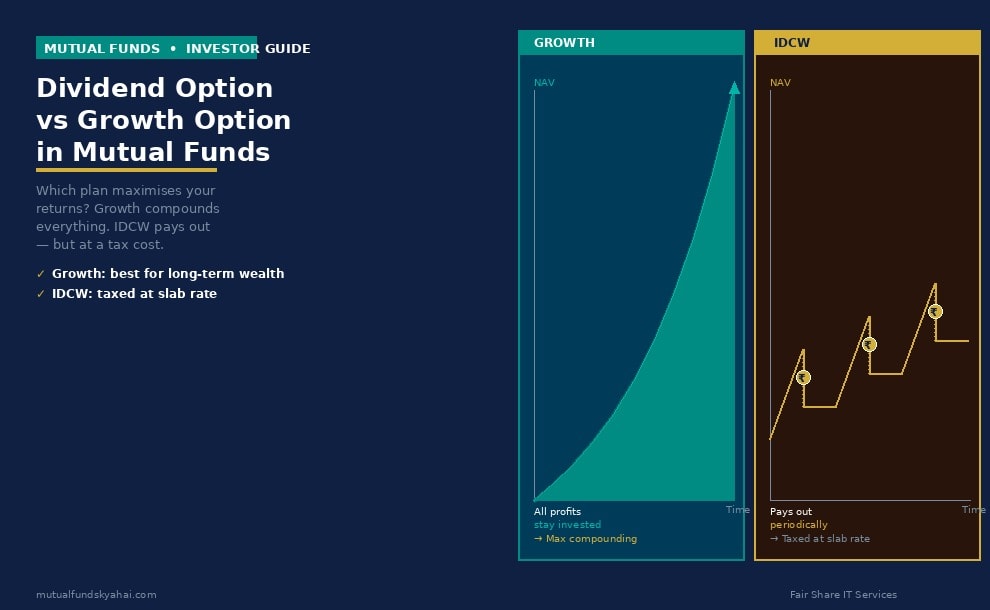

In the Growth Option, the profits earned by the mutual fund — whether through dividends from stocks, interest from bonds, or capital gains from selling securities — are reinvested back into the fund. No money is paid out to investors.

As a result, the NAV (Net Asset Value) of the fund grows over time, reflecting the cumulative effect of all reinvested profits. When you eventually redeem your units, you receive a lump sum that includes your original investment plus all the growth that has compounded over the years.

Example: Suppose you invest ₹1,00,000 in a Growth Plan at a NAV of ₹100 (1,000 units). Over five years, the NAV rises to ₹180. Your investment is now worth ₹1,80,000 — purely through NAV appreciation, with no payouts in between.

How Does the IDCW (Dividend) Option Work?

In the IDCW Option, the fund periodically distributes a portion of its profits to investors as income distributions. These payouts are not guaranteed — the fund's trustees decide the frequency and amount based on distributable surplus. Common frequencies are monthly, quarterly, or annual.

Crucially, when a distribution is made, the NAV of the fund drops by exactly the amount distributed per unit. So if the NAV is ₹30 and the fund pays ₹2 per unit, the NAV falls to ₹28 after the payout. This is why IDCW payouts are sometimes misunderstood as "free money" — they are actually a return of your own accumulated value.

Example: You invest ₹1,00,000 in an IDCW Plan at NAV ₹100. After a year, the NAV rises to ₹115. The fund declares a distribution of ₹10 per unit, so you receive ₹10,000 in your bank account. But the NAV falls to ₹105. Your total wealth remains ₹1,05,000 + ₹10,000 = ₹1,15,000 — the same as the Growth Plan, before taxes.

Key Differences: Growth vs IDCW at a Glance

- NAV behaviour: Growth NAV compounds upward; IDCW NAV resets downward after each payout.

- Cash flow: Growth provides no periodic income; IDCW provides regular (but not guaranteed) payouts.

- Compounding: Growth maximises compounding because profits stay invested; IDCW breaks the compounding cycle with each payout.

- Taxation: This is where the difference becomes most significant (see below).

Tax Treatment: The Most Important Difference

As of FY 2025–26, the tax treatment for these two options differs substantially:

Growth Option — Capital Gains Tax on Redemption

When you redeem Growth Plan units, the profit is taxed as capital gains. For equity mutual funds held for more than 12 months, Long-Term Capital Gains (LTCG) above ₹1.25 lakh are taxed at 12.5% (as per current rates). Short-term gains (held under 12 months) are taxed at 20%. You pay tax only when you redeem — giving you full control over the timing.

IDCW Option — Tax in the Year of Receipt

IDCW payouts are added to your total income for the year and taxed at your applicable income tax slab rate. If you are in the 30% tax bracket, every IDCW payout is taxed at 30% — far higher than the LTCG rate. Additionally, TDS (Tax Deducted at Source) at 10% is deducted if the payout exceeds ₹5,000 in a financial year.

This makes the IDCW option significantly less tax-efficient for most investors, particularly those in higher tax brackets or those who do not need regular cash flow.

Who Should Choose the Growth Option?

The Growth Option is generally the better choice for:

- Long-term wealth creators: Investors with a 5–10+ year horizon who want to maximise compounding.

- Younger investors: Those who do not need periodic income and can reinvest all returns.

- Higher tax bracket investors: The LTCG tax rate is lower than slab-rate taxation on IDCW payouts.

- Goal-based investors: Those saving for retirement, children's education, or a home purchase.

Who Should Consider the IDCW Option?

The IDCW Option may be suitable in limited scenarios:

- Retirees or those needing regular income: If you depend on monthly or quarterly payouts for living expenses and have no other income source.

- Lower tax bracket investors: If you are in the 0% or 5% tax slab, the tax impact of IDCW payouts is minimal.

- Debt fund investors seeking regular income: Some debt fund IDCW options offer more predictable distributions, though the tax treatment applies equally.

Important note: Even for retirees, a Systematic Withdrawal Plan (SWP) from the Growth Option is often a more tax-efficient and reliable way to generate regular income than the IDCW Option.

Why SEBI Renamed "Dividend Option" to "IDCW"

SEBI mandated the rename in 2021 to prevent investors from confusing mutual fund distributions with company dividends. A company dividend is paid out of corporate profits without affecting the share price. A mutual fund "dividend" (now IDCW) is simply a redistribution of the fund's NAV — no new value is created. The new name, Income Distribution cum Capital Withdrawal, more accurately describes what happens: part of the distribution may come from the investor's own accumulated capital, not just income earned by the fund.

Key Things to Watch Out For

- IDCW is not guaranteed: Fund houses can skip distributions if the portfolio does not generate sufficient distributable surplus. Never rely on IDCW as a fixed income source.

- NAV illusion: A lower NAV in the IDCW plan does not mean the fund is "cheaper." It simply reflects past distributions. Always compare total returns, not NAV alone.

- Wrong plan for SIP investors: Choosing IDCW in a long-term SIP completely defeats the purpose of compounding. For SIPs, Growth is almost always the right choice.

- Tax drag compounds over time: Even a small annual tax on IDCW payouts significantly erodes your terminal corpus over 10–15 years compared to the Growth Option.

- Check your direct vs regular plan too: The Growth/IDCW choice applies to both Direct and Regular plans. Make sure you also choose the Direct Plan to avoid paying distributor commission.

Frequently Asked Questions

Can I switch from IDCW to Growth Option?

Yes. Most fund houses allow you to switch between options within the same scheme. However, this is treated as a redemption followed by a fresh purchase, so it may trigger capital gains tax. Check the exit load period and your holding tenure before switching.

Is IDCW reinvestment the same as Growth Option?

No. Some fund houses offer an IDCW Reinvestment sub-option, where the payout is reinvested back into the fund as fresh units. This partially mimics the Growth Option, but the tax on each distribution is still triggered, making it less efficient than a true Growth plan.

Which option is better for ELSS (tax-saving) funds?

For ELSS funds, the Growth Option is strongly preferred. The 3-year lock-in period means you cannot redeem anyway, so receiving IDCW payouts that are fully taxable at your slab rate makes little financial sense. Growth lets the corpus compound fully over the lock-in period.

Does the fund's performance differ between Growth and IDCW plans?

No. Both plans invest in the same underlying portfolio and are managed identically. The only difference is how profits are handled. Performance comparisons between the two options of the same scheme should be made on a total return basis, not on NAV alone.