What is TER (Total Expense Ratio) in Mutual Funds?

The Total Expense Ratio (TER) is the annual fee that a mutual fund charges its investors to cover all operating costs — fund management, administration, marketing, distribution, registrar and transfer agent fees, custodian fees, and audit charges. It is expressed as a percentage of the fund's daily average net assets and is deducted from the fund's NAV every single day, invisibly.

In simple terms, TER is the all-in cost of owning a mutual fund. Unlike a brokerage or a fixed fee you pay upfront, TER is silently deducted from your returns every year. The NAV you see published every evening is already net of TER — meaning the fund's stated return is after the TER has been taken out.

SEBI mandates that every mutual fund scheme disclose its TER clearly on the fund's website and in its Scheme Information Document (SID). Investors have a right to know exactly how much they are paying.

How Does TER Work? A Step-by-Step Example

Suppose you invest ₹1,00,000 in a mutual fund with a TER of 1.5% per year. The fund generates a gross return of 12% in the year.

- Gross return on ₹1,00,000 = ₹12,000

- TER charged = 1.5% of average corpus ≈ ₹1,500

- Net return to you = ₹12,000 − ₹1,500 = ₹10,500 (10.5%)

The fund would report its NAV-based return as 10.5%, not 12% — you never see the 1.5% deducted as a separate line item. It is embedded in the NAV calculation daily, at a rate of roughly TER ÷ 365 per day.

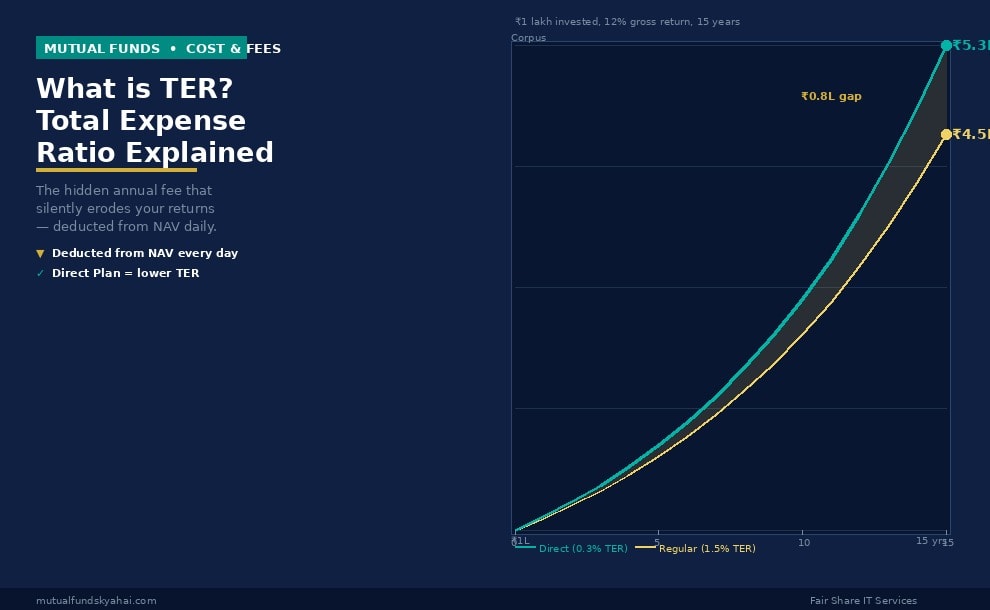

Now consider the long-term compounding impact. If two funds both earn 12% gross over 20 years but one has a TER of 0.5% (Direct Plan) and the other 1.75% (Regular Plan), a ₹1,00,000 investment grows to approximately ₹8.6 lakh vs ₹6.5 lakh respectively — a difference of over ₹2 lakh, purely from the TER gap.

SEBI's TER Limits: What the Regulator Allows

SEBI regulates the maximum TER a fund can charge, with limits based on assets under management (AUM). As of current SEBI regulations (effective October 2018 and revised thereafter), the limits for equity and debt funds follow a slab structure:

- First ₹500 crore of AUM: Up to 2.25% (equity) / 2.00% (debt)

- Next ₹250 crore: Up to 2.00% (equity) / 1.75% (debt)

- Next ₹1,250 crore: Up to 1.75% (equity) / 1.50% (debt)

- Next ₹3,000 crore: Up to 1.60% (equity) / 1.35% (debt)

- Beyond ₹50,000 crore: Up to 1.05% (equity) / 0.80% (debt)

This means larger funds benefit from economies of scale, and the TER naturally tends to decrease as a fund's AUM grows. Index funds and ETFs, being passively managed, are required to have even lower TERs — often under 0.5% for popular Nifty 50 or Sensex index funds.

Direct Plan vs Regular Plan: The TER Difference That Matters Most

Every mutual fund scheme in India offers two variants — Direct Plan and Regular Plan. The TER difference between them is one of the most important financial decisions an investor makes.

Regular Plan: Includes distributor commission in the TER. When you invest through a bank, broker, or financial advisor, they receive a trail commission from the AMC, which is built into the TER. Regular Plan TERs are typically 0.5% to 1.25% higher than Direct Plans.

Direct Plan: No distributor commission is paid. The full returns (after fund management and operational costs) accrue to you. Direct Plan NAVs are therefore always higher than Regular Plan NAVs for the same scheme.

For a long-term SIP investor, this difference compounds significantly. A 1% lower TER in the Direct Plan, sustained over 15–20 years, can add lakhs to your terminal corpus — making the choice of Direct vs Regular one of the highest-impact decisions in personal finance.

Types of Costs Included in TER

The TER is an umbrella figure that bundles several charges:

- Investment management fee: Paid to the fund manager and the AMC's investment team — typically the largest component.

- Administrative costs: Office expenses, IT systems, compliance, legal, and audit costs.

- Registrar and Transfer Agent (RTA) fee: Paid to RTAs like CAMS or KFintech for maintaining investor records and processing transactions.

- Custodian fee: Paid to the bank or financial institution that holds the fund's securities in safe custody.

- Marketing and distribution costs: Present only in Regular Plans; covers trail commissions to distributors.

- Statutory levies: SEBI turnover fees and GST on investment management fees.

Importantly, brokerage costs incurred when the fund buys or sells securities are not included in the TER — they are charged directly to the scheme separately.

Who Should Pay Special Attention to TER?

TER matters for every mutual fund investor, but it is most critical for:

- Long-term SIP investors: The compounding effect of TER over 10–20 years is enormous. Even 0.5% matters at long horizons.

- Debt fund investors: Debt funds generate modest returns of 6–8%. A TER of 1.5% erodes 15–20% of the gross return — far more painful than in equity funds generating 12%+.

- Index fund and ETF investors: The entire investment philosophy of passive investing depends on low TER. A Nifty 50 index fund with 0.1% TER vs 0.5% TER makes a material difference over time.

- Large lump-sum investors: The bigger your corpus, the more rupees you lose in absolute terms for every percentage point of TER.

Key Things to Watch Out For

- Don't compare TERs across fund categories: A 1.8% TER for a small-cap fund is very different from 1.8% for a liquid fund. Compare within categories only.

- TER can change: AMCs can revise TER within SEBI limits. A fund that charged 1.2% last year may charge 1.5% this year. Check the current TER on the AMC website before investing.

- Lower TER ≠ better fund: A well-managed active fund with 1.8% TER may still outperform an index fund with 0.1% TER. Focus on risk-adjusted returns after TER, not TER alone.

- TER is not exit load: Exit load is a one-time penalty on early redemption, separate from TER. They are often confused but are entirely different charges.

- Check the factsheet: SEBI requires AMCs to publish the current TER in the monthly factsheet and on their website. Always verify before investing.

Frequently Asked Questions

Is TER charged on the invested amount or the total portfolio value?

TER is charged on the scheme's daily average net assets — that is, the current market value of all investments held, not just the amount you originally invested. As your portfolio grows, the absolute rupee amount deducted increases each year, even if the percentage remains constant.

How do I find the TER of a mutual fund?

The current TER is disclosed on the AMC's official website, AMFI's website (amfiindia.com), and in the scheme's monthly factsheet. It is also published in the Scheme Information Document (SID). Look for the "TER" or "Expense Ratio" row in the scheme details section.

Is a lower TER always better for an active fund?

Not necessarily. For active funds, the fund manager's skill in generating alpha (returns above the benchmark) is also critical. A fund with 2% TER that consistently delivers 15% net returns beats a fund with 1% TER delivering 10%. However, for passive funds (index funds, ETFs), where returns closely track the index, a lower TER is almost always better, as there is no scope for manager skill to compensate.

Can the TER go above the SEBI-specified limit?

No. SEBI's TER limits are hard caps. An AMC cannot charge investors more than the prescribed maximum for any scheme category. However, the limits vary by AUM slab, and AMCs can charge up to the maximum allowed for their fund's AUM bracket. Investors can check SEBI's circular on TER for the latest applicable limits.