You invest ₹1 lakh in a mutual fund. The fund delivers 12% returns that year. But when you check your actual gains, they are slightly lower. You wonder why. The answer, in most cases, is the expense ratio — a small but powerful number that quietly reduces your returns every single day.

What is Expense Ratio?

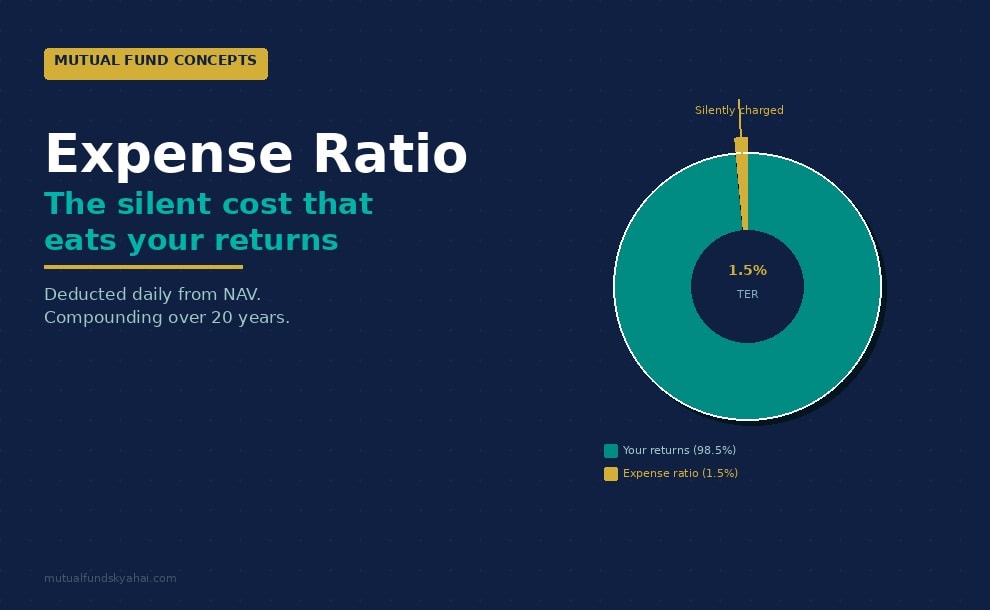

The expense ratio is the annual fee that a mutual fund charges to manage your money. It is expressed as a percentage of the fund's average daily net assets. This fee covers the fund manager's salary, administrative costs, marketing expenses, distributor commissions, and other operational costs of running the fund.

The expense ratio is not deducted from your account directly. Instead, it is built into the Net Asset Value (NAV) of the fund. Every day, a tiny fraction of the total expense ratio is deducted from the fund's assets before the NAV is published. So the NAV you see is already net of the expense ratio — you never receive a separate bill, but you are paying it silently, every day.

How is Expense Ratio Calculated?

The formula is straightforward:

Expense Ratio = Total Annual Fund Expenses ÷ Average Daily Net Assets × 100

For example, if a fund has ₹1,000 crore in assets and its total annual operating expenses are ₹15 crore, the expense ratio is 1.5%.

On a daily basis, this translates to about 0.004% per day (1.5% ÷ 365), which is deducted from the fund's assets before the NAV is published. Over time, this compounding deduction can significantly impact your wealth.

What Does SEBI Say About Expense Ratio?

SEBI (Securities and Exchange Board of India) regulates the maximum expense ratio mutual funds can charge. The limits are tiered — funds with larger assets under management (AUM) must charge lower expense ratios. As of recent guidelines:

- For the first ₹500 crore of AUM: maximum 2.25% (equity) / 2.00% (debt)

- For the next ₹250 crore: maximum 2.00% (equity) / 1.75% (debt)

- Beyond ₹1,000 crore: progressively lower caps apply

- Direct plans must have a lower expense ratio than regular plans — the difference is roughly the distributor commission

The expense ratio is also called the Total Expense Ratio (TER) in regulatory filings.

Direct Plan vs Regular Plan — The Expense Ratio Difference

One of the most important decisions an investor makes is choosing between a direct plan and a regular plan of the same mutual fund. The only real difference between the two is the expense ratio:

- Regular plan: Includes a distributor commission (typically 0.5–1.5%) in the expense ratio. If you invest through a broker, bank, or distributor, you are in the regular plan.

- Direct plan: No distributor commission. Lower expense ratio — typically 0.5–1% lower than the regular plan of the same fund.

Over 20 years, a difference of just 1% per year in expense ratio can mean a difference of 15–20% in your final corpus. For a ₹10 lakh investment, that could be ₹1.5–2 lakh in extra wealth — simply by choosing the direct plan.

What is a Good Expense Ratio?

- Index funds / ETFs: 0.05%–0.25% is considered excellent. These are passively managed and have very low costs.

- Actively managed equity funds: 0.5%–1.5% is reasonable for a direct plan. Above 1.5% starts eating significantly into returns.

- Debt funds: 0.1%–0.5% for direct plans. Debt returns are lower than equity, so a high expense ratio hurts proportionately more.

- Liquid funds: Below 0.3% is normal. Even 0.5% would be high for a liquid fund yielding ~7%.

How Expense Ratio Impacts Long-Term Returns

The effect of expense ratio compounds silently over time. Consider this illustration:

- Investment: ₹10 lakh over 20 years

- Gross return: 12% per annum

- Fund A (expense ratio 0.5%): Net return ~11.5%. Final corpus: ~₹86 lakh

- Fund B (expense ratio 2.0%): Net return ~10%. Final corpus: ~₹67 lakh

The difference of just 1.5% in expense ratio results in ₹19 lakh less in your pocket — on the same ₹10 lakh investment. This is why Warren Buffett famously recommends low-cost index funds for most investors.

Frequently Asked Questions

Is a lower expense ratio always better?

Generally yes — all else being equal, a lower expense ratio means more of the fund's returns flow to you. However, a skilled active fund manager who consistently beats the benchmark may justify a higher expense ratio. Always compare net returns, not just expense ratios in isolation.

How do I check a fund's expense ratio?

You can find the current TER on AMFI's website (amfiindia.com), on the fund house's own website, or on platforms like Zerodha Coin, Groww, or MFCentral. SEBI requires all AMCs to update their TER daily.

Does expense ratio change over time?

Yes. As a fund's AUM grows, its expense ratio can decrease (since fixed costs are spread over more assets). SEBI also revises its TER limits periodically. You should check the current expense ratio before investing, not just when you first researched the fund.

Is the expense ratio charged even when the fund is losing money?

Yes. The expense ratio is charged regardless of fund performance. In a year when the fund loses 10%, you effectively lose 10% plus the expense ratio. This is why selecting a low-cost fund is especially important during volatile markets.