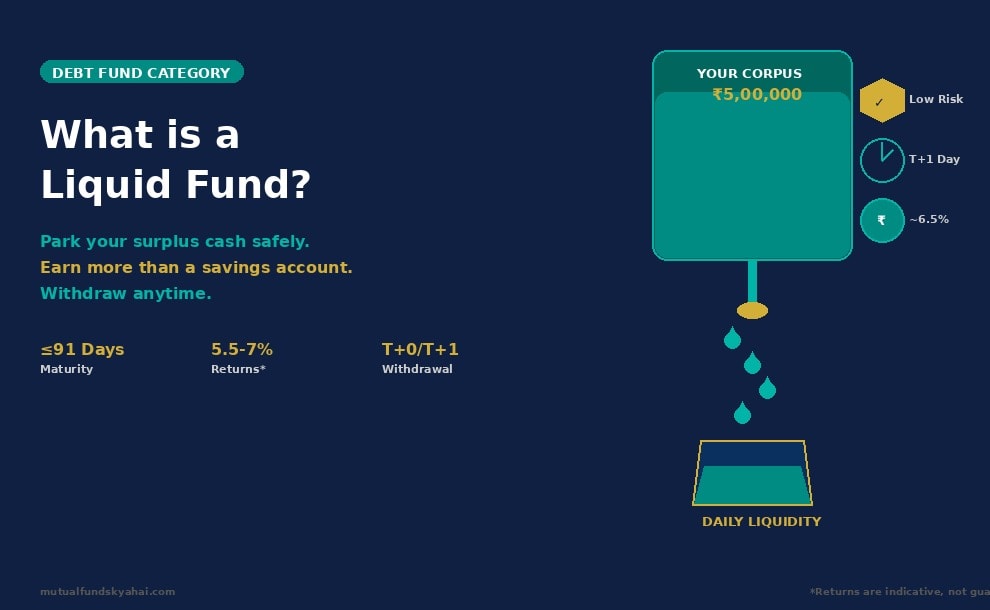

What is a Liquid Fund?

A liquid fund is a type of debt mutual fund that invests in very short-term money market instruments — such as treasury bills, commercial paper, certificates of deposit, and term deposits — with a residual maturity of up to 91 days. Because the underlying securities mature so quickly, liquid funds carry very low interest rate risk and offer high liquidity, which is why they are called "liquid" in the first place.

Think of a liquid fund as a smarter version of your savings account. Your money is not locked in. You can withdraw it on any business day, and in many cases, receive the redemption amount in your bank account within 24 hours or even on the same day through instant redemption facilities (up to ₹50,000 per day per scheme).

How Does a Liquid Fund Work?

When you invest in a liquid fund, the fund manager pools your money with that of other investors and deploys it into high-quality, short-duration debt instruments. These instruments are issued by the government, banks, and large corporations, and they mature within a few weeks to a few months.

Because the investments are so short-term, the fund's NAV (Net Asset Value) moves very gradually. Unlike equity funds where the NAV can swing 2-3% in a single day, a liquid fund's NAV typically changes by tiny fractions — making it one of the most stable categories in the entire mutual fund universe.

Here is a simple illustration. Suppose you park ₹5,00,000 in a liquid fund that delivers an annualised return of 6.5%. After 90 days, your investment would grow to approximately ₹5,08,014 — before tax. Compare this to a regular savings account offering 3-4% interest, and you can see why liquid funds are attractive for short-term parking of surplus cash.

One important feature: liquid funds do not have any lock-in period. However, if you redeem your units within 7 days of purchase, an exit load of up to 0.0070% may be charged on a graded basis, as per SEBI regulations. After 7 days, there is no exit load at all.

What Do Liquid Funds Invest In?

The portfolio of a typical liquid fund includes a mix of the following instruments, all maturing within 91 days:

Treasury Bills (T-Bills): Short-term government securities considered virtually risk-free. They are issued by the Reserve Bank of India on behalf of the Government of India.

Commercial Paper (CP): Unsecured, short-term promissory notes issued by well-rated corporations to meet their working capital needs. The credit quality of the issuer matters here.

Certificates of Deposit (CD): Time deposits issued by scheduled commercial banks. These are negotiable and carry relatively low credit risk.

Collateralised Borrowing and Lending Obligations (CBLO) / Tri-party Repo: Overnight or very short-term lending instruments used in the interbank market, backed by government securities as collateral. These are among the safest instruments in a liquid fund portfolio.

Term Deposits: Fixed deposits placed with banks for short durations.

Who Should Consider Investing in a Liquid Fund?

Liquid funds are not meant for long-term wealth creation. They serve a very specific purpose — parking money safely for short periods while earning better returns than a savings account. Here are the investor profiles that benefit most:

Emergency fund builders: If you are setting aside 3-6 months of expenses as an emergency corpus, a liquid fund is an excellent place to keep it. Your money stays accessible, and it earns more than a savings account.

Investors waiting to deploy into equity: If you have received a lump sum — say a bonus or inheritance — and want to invest it in equity via STP (Systematic Transfer Plan), you can park the lump sum in a liquid fund first and gradually transfer it into an equity fund over a few months.

Business owners managing cash flow: Companies and small business owners often use liquid funds to park surplus operating cash that they will need within weeks or months.

Short-term goal savers: If you have a planned expense coming up in 1-3 months — such as an insurance premium, a vacation, or a down payment — a liquid fund lets you earn a small return on that money instead of leaving it idle in a current account.

Liquid Fund vs Savings Account vs Fixed Deposit

Many investors wonder how liquid funds compare to traditional banking products. Here is a practical comparison:

Returns: Savings accounts typically offer 3-4% per annum. Fixed deposits for 3 months may offer 5-6%. Liquid funds have historically delivered 5.5-7% annualised returns, though these are market-linked and not guaranteed.

Liquidity: Savings accounts offer instant access. Liquid funds offer T+1 redemption (next business day) for amounts above ₹50,000, and instant redemption up to ₹50,000 per scheme per day. FDs have a penalty for premature withdrawal.

Taxation: Interest from savings accounts above ₹10,000 per year is taxable. FD interest is fully taxable as per your income slab. Liquid fund gains are also taxed as per your income tax slab if held for less than 3 years, but you benefit from the ability to time your redemption and manage your tax liability better.

Risk: Savings accounts and FDs (up to ₹5 lakh) are covered by DICGC insurance. Liquid funds carry a very small but non-zero credit risk. In rare cases, a default by an issuer of commercial paper can affect the fund's NAV. SEBI has tightened regulations significantly after the 2019 credit events to make liquid funds safer.

Key Things to Watch Out For

Credit quality matters: Always check the portfolio of the liquid fund before investing. Prefer funds that invest predominantly in sovereign (government) securities and AAA-rated instruments. Avoid funds that chase higher returns by taking on lower-rated credit exposure.

Check the expense ratio: Since returns from liquid funds are already modest (5.5-7%), a high expense ratio can eat into your gains significantly. Direct plans have lower expense ratios than regular plans — the difference is typically 0.15-0.30% — and this matters in a low-return category like liquid funds.

Do not use liquid funds for long-term investing: If your investment horizon is more than 6-12 months, consider other debt fund categories like short duration funds or corporate bond funds that may offer higher yields, albeit with slightly more risk.

NAV calculation is different: Unlike other mutual fund categories where the purchase NAV is based on the day you invest, liquid fund purchases are allotted at the next day's NAV if the application is received after 1:30 PM. If received before 1:30 PM, the same day's NAV applies.

SEBI's mark-to-market rule: Since 2020, SEBI requires liquid funds to mark all their securities to market value daily (previously, some securities were valued at amortised cost). This makes NAV movements more transparent but can occasionally cause very minor fluctuations.

Frequently Asked Questions

Are liquid funds safe?

Liquid funds are among the safest mutual fund categories, but they are not risk-free. The main risks are credit risk (default by an issuer) and liquidity risk (difficulty selling securities during market stress). SEBI has imposed strict regulations — including mandatory mark-to-market valuation, graded exit loads for early redemption, and caps on sector exposure — to minimise these risks. For most retail investors, liquid funds from reputable AMCs with conservative portfolios are considered a safe parking option.

What is the minimum investment in a liquid fund?

Most liquid funds allow you to start with as little as ₹500 to ₹1,000 for a lump sum investment. There is no maximum limit. SIP investments are also available, though most investors use liquid funds for lump sum parking rather than systematic investing.

Can I lose money in a liquid fund?

While extremely rare, yes — it is possible to see a temporary dip in the NAV of a liquid fund, especially if one of the underlying securities faces a credit event. However, over any 30-day or longer period, liquid funds have historically delivered positive returns. The risk of capital loss is significantly lower than in any other mutual fund category.

How are liquid fund returns taxed in India?

For investments held less than 3 years, gains from liquid funds are added to your income and taxed as per your applicable income tax slab. For investments held longer than 3 years, gains were previously taxed at 20% with indexation benefit, but recent tax changes have removed indexation for debt funds purchased after April 2023. It is advisable to consult a tax professional for the latest rules applicable to your situation.